America’s Affordable Housing Problem

America’s Affordable Housing Problem

The Problem

Housing in America is expensive. Just ask your average American. Nearly 42% of U.S. households spend 35% or more of their income on rent1. This leaves households with less money for other vital costs like healthcare, food, transportation, and savings, and makes them especially vulnerable to economic shocks. Rent growth has far exceeded income growth in recent years which is one of the reasons making it increasingly more difficult for people to save up and purchase a home let alone just be able to rent from one.

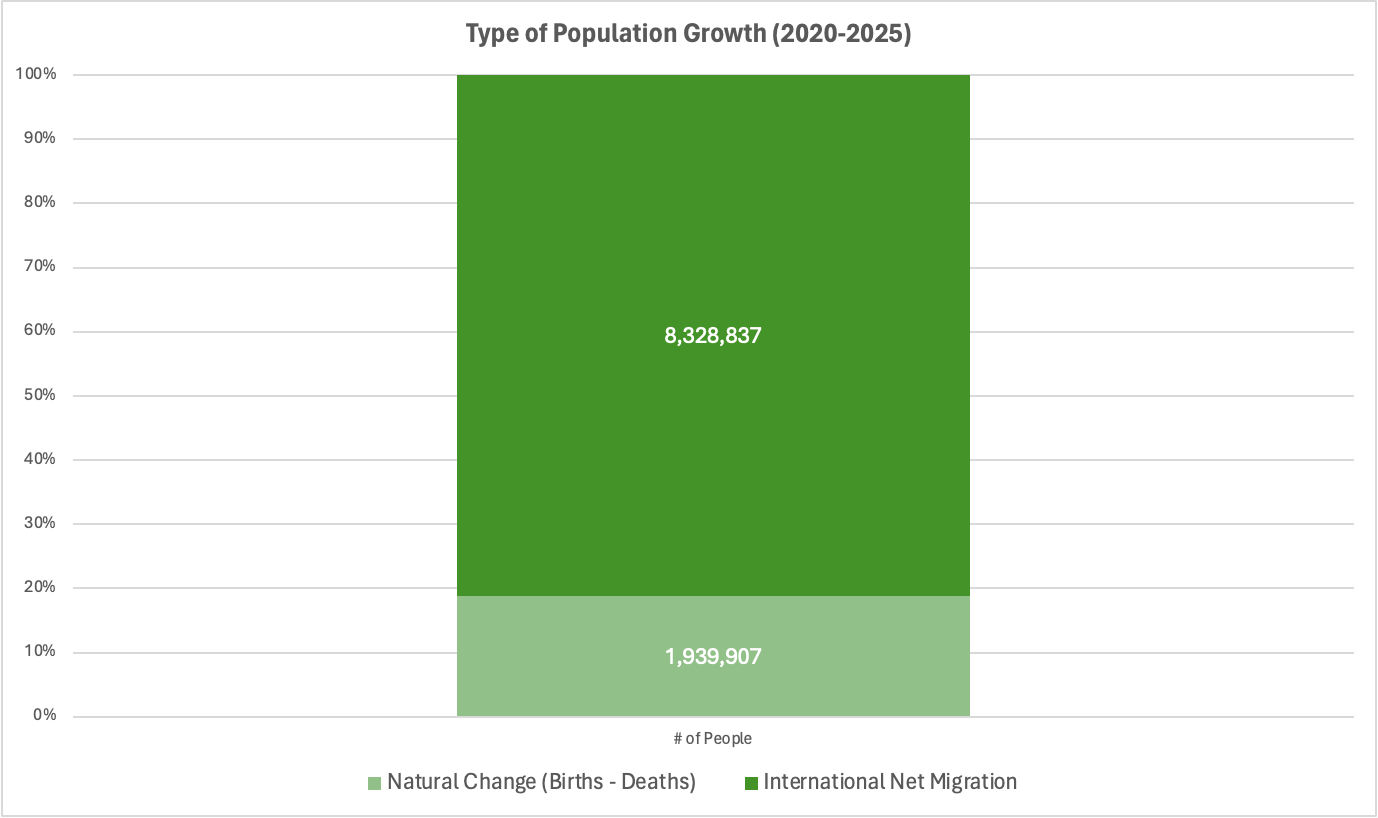

In addition to rents outpacing income growth, population growth has added further strain to housing affordability. Over the past five years (2020-2025), the United States has added more than 10 million residents. Of this increase, roughly 81% is attributable to net international migration, while only 19% stems from natural population change—births minus deaths2. While controlled immigration is generally a positive force for economic expansion, it would not be honest to ignore the short-term pressures and adjustment costs that accompany rapid demographic change, particularly in housing markets with already constrained supply.

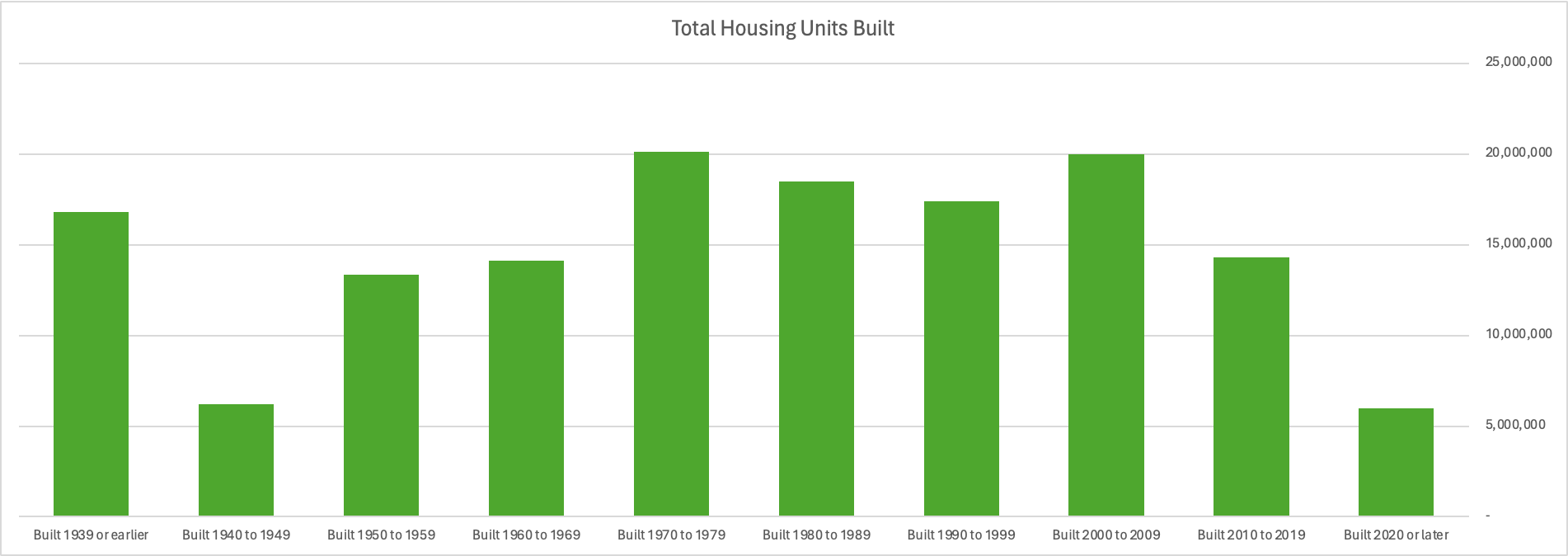

So if rent growth has outpaced income growth, and the population has continued to increase, if more homes were built, wouldn’t that help solve the problem? The number of housing units built each year over the past 20 years has seen anemic growth, and especially so in recent years3. The reasons are numerous: restrictive zoning laws, environmental regulations, administrative delays, rising property taxes, increasing construction costs, higher interest rates, and growing labor constraints, among others. Individually, each factor slows development, and cumulatively makes the process nearly unattainable at scale.

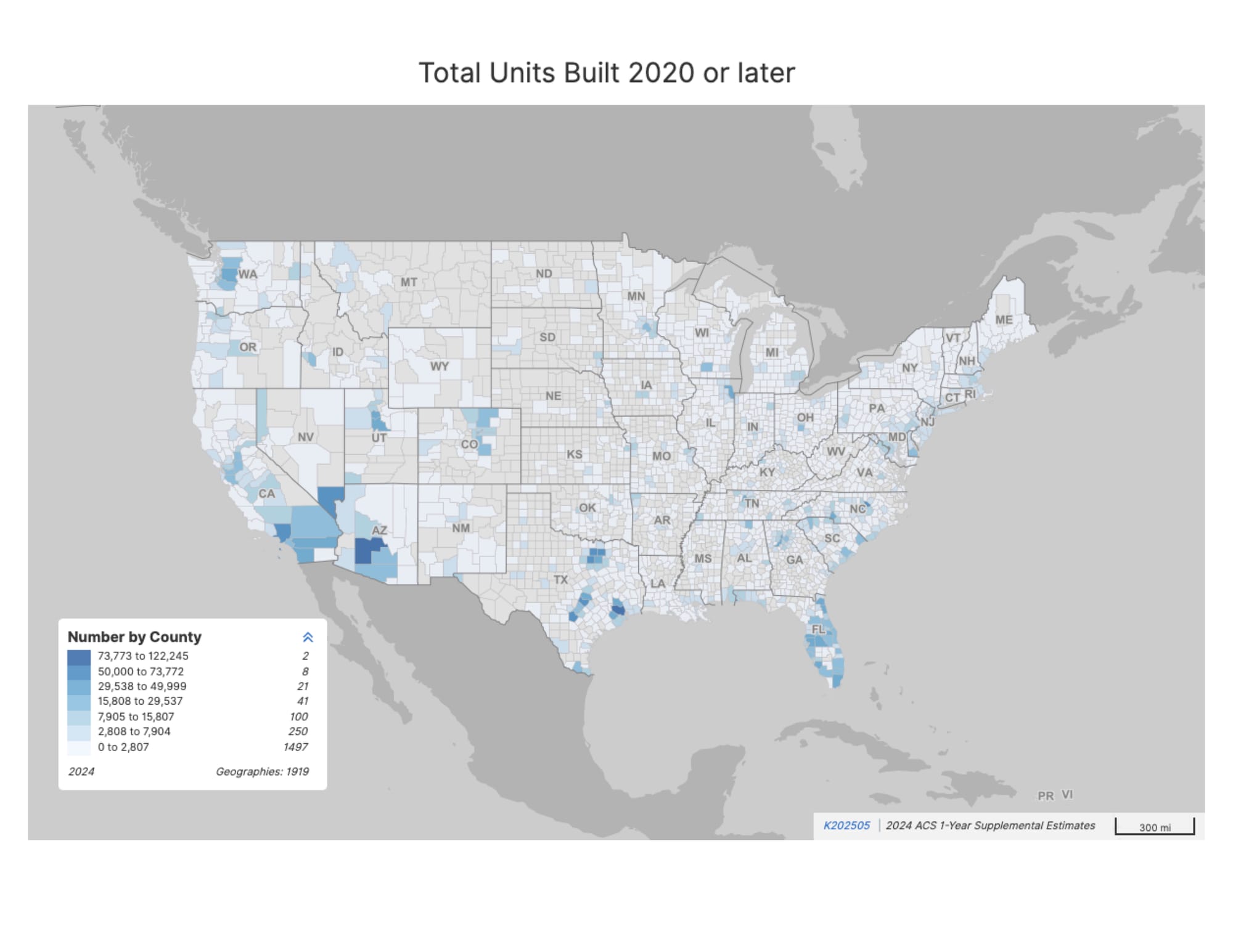

According to 2024 ACS estimates, only ten counties have produced over 50,000 housing units since 20204. While counties require various needs of housing supply due to their own individual population growth, the truth remains that housing supply has not kept on par with the growing demand.

The Current Solutions

Recognizing that market forces alone are often insufficient to produce housing affordable to low- and moderate-income households, the government has historically relied on two primary policy tools to address the affordability gap: rental assistance and development incentives. Chief among these are the section 8 housing assistance program, the low-income housing tax credit program, and tax-exempt bonds.

While structurally different, yet often paired together, these programs share a common goal: to reduce the gap between what households can afford to pay and what it costs to build and operate housing. However, with development gaps continuing to increase, competition to access governmental subsidies has gotten ever more competitive.

With that said, the recent passing of the One Big Beautiful Bill (“OBBB”) helped reduced the amount of private activity bonds required to finance an affordable housing developments. Previously, the test was 50% of the projects costs and land needed to be financed with private activity bonds, now it is only 25%. This allows for more projects to access private activity bonds because developments now require half of what they used to in order to develop affordable housing. In theory this will essentially double the amount of housing supply that is developed with tax-exempt bonds. With that said, doubling the amount of projects being built means investors are in theory also seeing twice the amount of deals which is putting downward pressure on tax credit equity pricing. Additionally, the OBBB permanently increases 9% LIHTC allocations by 12%, expanding the supply of tax credits in what has historically been an intensely competitive 9% LIHTC environment.

What Lies Ahead

The Affordable Housing Credit Improvement Act (“AHCIA”) which was originally introduced in 2016, and recently reintroduced in 2025, aims to build on some of provisions partially implemented in the OBBB. A detailed summary of the provision and improvements can be seen here. In addition to federal legislation, states have taken matters into there own hand. An example of this is the most recent proposal of SB 417 in California, a $10 billion dollar housing bond that would help expand homeownership, rental affordable housing, and shelters for those experiencing homelessness.

Sources

- U.S. Census Bureau. "Selected Housing Characteristics." American Community Survey, ACS 1-Year Estimates Data Profiles, Table DP04, https://data.census.gov/table/ACSDP1Y2024.DP04?t=Financial+Characteristics&moe=false. Accessed on 16 Feb 2026.

- Annual and Cumulative Estimates of the Components of Resident Population Change for the United States, Regions, States, District of Columbia, and Puerto Rico: April 1, 2020 to July 1, 2025 (NST-EST2025-COMP), Source: U.S. Census Bureau, Population Division, Release Date: January 2026

- U.S. Census Bureau. "Year Structure Built." American Community Survey, ACS 1-Year Estimates Detailed Tables, Table B25034, https://data.census.gov/table/ACSDT1Y2024.B25034?t=Year+Structure+Built&g=010XX00US. Accessed on 16 Feb 2026.

- U.S. Census Bureau. "Year Structure Built" American Community Survey, ACS 1-Year Supplemental Estimates, Table K202505, 2024, https://data.census.gov/table/ACSSE2024.K202505?q=K202505: Accessed on February 16, 2026.